As Portfolio Manager of the Milford Dynamic Small Companies Fund my focus is on smaller companies, and one of the consistent themes I’ve witnessed over the years is that founder-led, family-linked or employee-owned businesses often have an exceptional track record of outperformance. Back in August 2021 we first analysed the performance of these businesses against the broader market index. The results were stunning. The founder-led portfolio returned 41% p.a. over 3 years against the S&P/ASX Small Ordinaries index return of 9.2% p.a., an outperformance of 31.7% p.a.! Nearly three years later, with a more volatile market landscape, it’s a good opportunity to revisit the results.

The Dynamic Small Companies Fund currently has around 30% of the portfolio invested in founder-led or family-linked businesses, similar levels to when we last reviewed. Some of these companies include the likes of David Tudehope’s Macquarie Telecom (MAQ.ASX), Chris Hulls’ Life360 (360.ASX), Rajiv Jain’s GQG (GQG.ASX) and Ryan Stokes’ Seven Group (SVW.ASX).

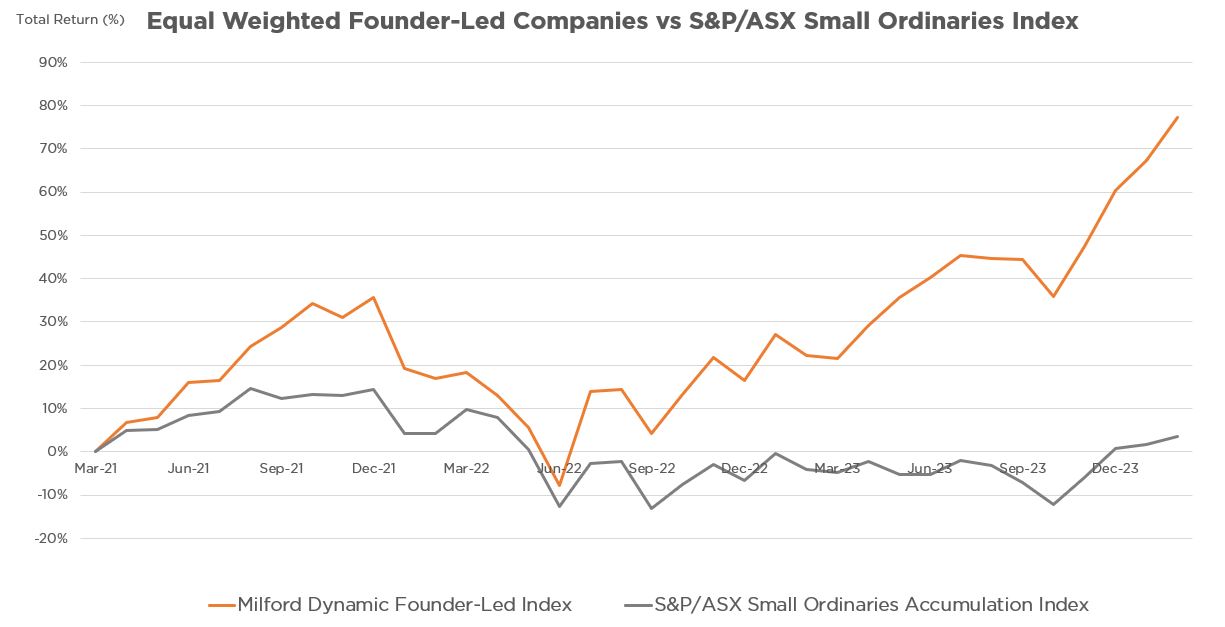

The data again confirmed why we love founder-led companies. The 3-year performance of the founder-led portfolio to April 2024 (23 companies) was 24.9% p.a. against the S&P/ASX Small Ordinaries index return of 2.7% p.a., an outperformance of 22.2% p.a.!

Source: Milford/Bloomberg

Why is this so?

Companies with a founder who owns a material stake and who is still actively engaged in the business can often think and act differently to companies run by professional managers. So why do founder-led, family-linked or employee-owned companies deliver performance over the long term? We have identified three key differentiators:

i) Long-term mindset

Founders are looking at establishing the business in a multi-generational timescale. According to a 2018 report by PWC strategy & consulting arm, the average tenure of a CEO in Australia is only five years. This is not a very long time to grow and develop a company. Incentives are also typically associated with earnings performance over shorter time periods (1 – 3 years), which can encourage management to focus on short-term outcomes over positive long-term shareholder returns.

ii) Skin in the game

We believe having a founder’s money next to ours is very powerful. This makes for a real alignment of interests. I’m sure you’ve heard the saying “no one works as hard as the owner”. Where professional managers come and go over time, it’s the founder who is there, and leading it toward success. These founders derive meaning from the challenge, identity and ethos of their work and not necessarily from the incentive package the board’s remuneration committee has devised for them. It is this commitment that often leads to remarkable levels of performance.

iii) Soul in the game (emotional investment)

Founders often bring a passion to business. They are building a legacy, which requires long-term thinking. The most underestimated attribute we find is the broader love of the business and the intent to continue the success they’ve had into the future. As Warren Buffett says, “We’ve had terrific luck with the entrepreneurs who basically love their businesses the way I love Berkshire”.

While on aggregate our analysis shows these companies have typically outperformed the benchmark, it is by no means a flawless strategy. Our equal weighted portfolio had ~15% of founder-led companies trade lower over the 3-year time period. It’s important to remember that assessing management is just one of a number of tools we use to analyse companies. Business quality and durability, industry landscape, valuation and ESG factors are all critical to our process.

I believe that Milford shares many of the same attributes I have discussed. One of our core values is to align our success to the performance of our clients’ capital. As a company, Milford has significant staff ownership, and staff are only able to invest in Milford or its Funds.

Learn more about the Milford Dynamic Small Companies Fund

Additional Disclaimer:

Equity Trustees Limited ABN 46 004 031 298 AFSL 240975, is the Responsible Entity for the Dynamic Small Companies Fund

You should read the PDS & TMD available at https://milfordasset.com.au/document/dynamic-small-companies-fund-pds

For the full disclaimer please visit https://milfordasset.com.au/disclaimer-linkedin