Falling markets are never good as you are suffering losses in your portfolio which impact your long-term returns. Investors cannot change what happened yesterday and need to make decisions looking forward. Many investors are feeling nervous and wondering whether to sell, or new investors are wondering whether to invest or stay in cash. When thinking about that, investors should consider that lower markets can bring investors a silver lining in the form of cheaper assets, which increase your forward-looking returns from today’s starting point. Let’s look at a few simplistic examples.

If I can buy a property for $1m and it pays me an annual rental of $60,000 then I am getting a yield of 6%p.a. If that property value falls to $850,000 and my tenants are still paying $60,000 then I am getting a yield of 7%p.a. Would you rather own the property at $1m or $850k if you don’t plan to sell any time soon?

The same logic applies to equity and bond markets. If I own a share that trades at $20 per share and that company earns $1 per share in company profits, then it is trading on a 5% earnings yield and a price-to-earnings (PE) ratio of 20X. If that share price falls to $15 but the company can still earn $1 per share, my earnings yield is now 6.7% and the stock is trading on 15X price-to-earnings. Would you rather own that stock at $15 or $20?

If I owned a bond paying me a fixed rate of interest for the next five years and the underlying interest rates go up, my bond is worth less because that same bond if issued today would have to pay me a higher rate of interest. Wouldn’t you rather own the bond today at a cheaper price but paying a higher effective rate of interest?

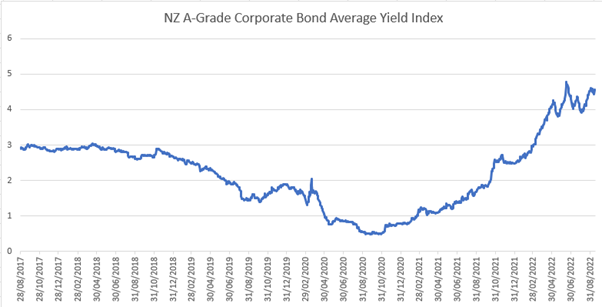

The examples above are not far from reality so far in 2022. Many share markets have fallen by around 20%, which is more than earnings have fallen, meaning you can now buy the markets on cheaper PE valuations and higher earnings yields. In fixed income markets, bond yields have gone up significantly, meaning capital values have fallen, but the yields you can now receive are the best they have been in years. The chart below shows the rise in yield on the NZ A-Grade Corporate Bond Index and as you can see, yields have gone from less than 1% to well over 4%.

Source: Bloomberg

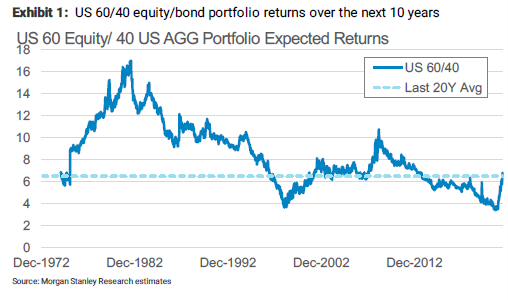

The chart below shows Morgan Stanley’s estimate of forward-looking returns over the next 10 years for a ‘balanced’ asset allocation of 60% US shares and 40% US Corporate Bonds. The chart is not a predictor of short-term returns, but as you can see, following the recent share market fall and the rise in bond yields, Morgan Stanley’s estimate of your forward looking 10-year returns has significantly improved to 6.6%, the highest expected level since 2014.

The analysis above is simplistic and should not be taken as a short-term view on markets, as share markets often fall because investors expect company earnings to fall. Currently there is an expectation that economies will slow (maybe even into recession), which will impact the company earnings outlook. So, while Milford is still relatively cautious on the near-term outlook, for those with a long-term investment time horizon, your chance of making better forward-looking returns has improved as assets have become cheaper. You don’t need to be adding to your investment directly to benefit from this situation. Milford’s Funds, through their active management, will take advantage on your behalf as we re-deploy some of the cash we have been holding to manage portfolios as markets have declined.

Weak markets can test investors’ nerves, and it is important to remind yourself of your long-term goals. During these difficult times it may be helpful to remember what the great investor Warren Buffett once said, “be fearful when others are greedy, and greedy when others are fearful”.